Interest deductibility rules for property investors detailed; 'New builds' to be exempt for 20 years

The Government has defined what it proposes will constitute a “new build” to be exempt from a major law change that prevents residential property investors from deducting interest as an expense when paying tax.

The Government proposes a property be considered “new” for 20 years from the time its code of compliance certificate is issued.

It proposes the exemption applies to properties that received this certificate on or after March 27, 2020, and the exemption applies to both the initial purchaser of the new build and any subsequent owner within the 20-year period.

It also proposes prefabricated houses and the conversion of existing dwellings into multiples dwellings be considered "new builds".

The Government is seeking feedback on whether the 20-year "new build" period should be extended for purpose-built rentals.

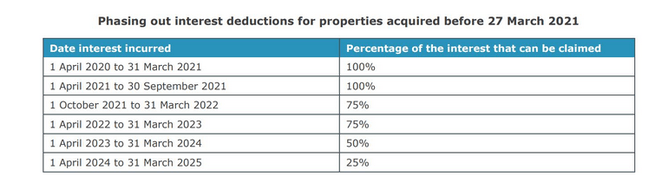

The removal of interest deductibility means that from October 1, 2021, interest will not be deductible for residential property acquired on or after March 27, 2021. For properties acquired before March 27, 2021, investors’ abilities to deduct interest will be phased out between October 1, 2021 and March 31, 2025.

Inland Revenue estimates the change will generate $80 million of tax revenue in the 2022 fiscal year, $200 million in 2023, $350 million in 2024, $490 million in 2025 and $650 million in 2026.

The Government in March announced the rule change. However, the change is only expected to be passed into law in early 2022. So, any details unveiled to date could technically be changed before then.

The rule change is set out in a Supplementary Order Paper (SOP) connected to a tax bill that’s just had its first reading in Parliament.

The SOP will go through the full select committee process, so the public will have an opportunity to provide feedback on it.

National and ACT have committed to reversing the change if elected into government.

Inland Revenue also said: "It is proposed that the interest limitation rules will not apply to most companies where their core business does not involve residential land. These are companies where residential property (including new builds) makes up less than half their total assets.

"Companies where five or fewer individuals or trustees own 50% or more of the company (referred to as close companies) will generally have to apply the rules even if their core business does not involve residential land. An exception is proposed for close companies that are Māori authorities or wholly-owned by a Māori authority."

See an easy-to-read facts sheet compiled by Inland Revenue here.

Article: Jenée Tibshraeny, www.interest.co.nz